Legal partner behind the builders of tomorrow. Mission

Pre-IPO Secondary Tokenisation After Anthropic and OpenAI: Why Issuer Recognition Matters

Summary: Anthropic and OpenAI have put unauthorised pre-IPO secondary exposure on notice: direct transfers, SPVs, tokenised interests, forwards and synthetic products cannot create recognised shareholder rights without issuer consent. Token platforms and structured-product arrangers need defensible upstream title or hedge, clear holder recourse and issuer-recognition risk disclosure before they can credibly distribute economic exposure to investors.

Authors:

Managing partner

Introduction – Why Pre-IPO Stock Tokens Are Not Just “Private Shares On-Chain”

Private-company secondaries have become one of the most aggressive corners of the pre-IPO market. The demand is simple: investors want access to OpenAI, Anthropic, SpaceX, xAI, Stripe, Neuralink and other private companies before IPO, while founders, employees and early investors hold valuable but illiquid shares. Tokenisation enters as a distribution layer on top of that market: it promises fractional access, broader investor reach, faster secondary trading and on-chain settlement for exposure that would otherwise remain private, negotiated and difficult to transfer.

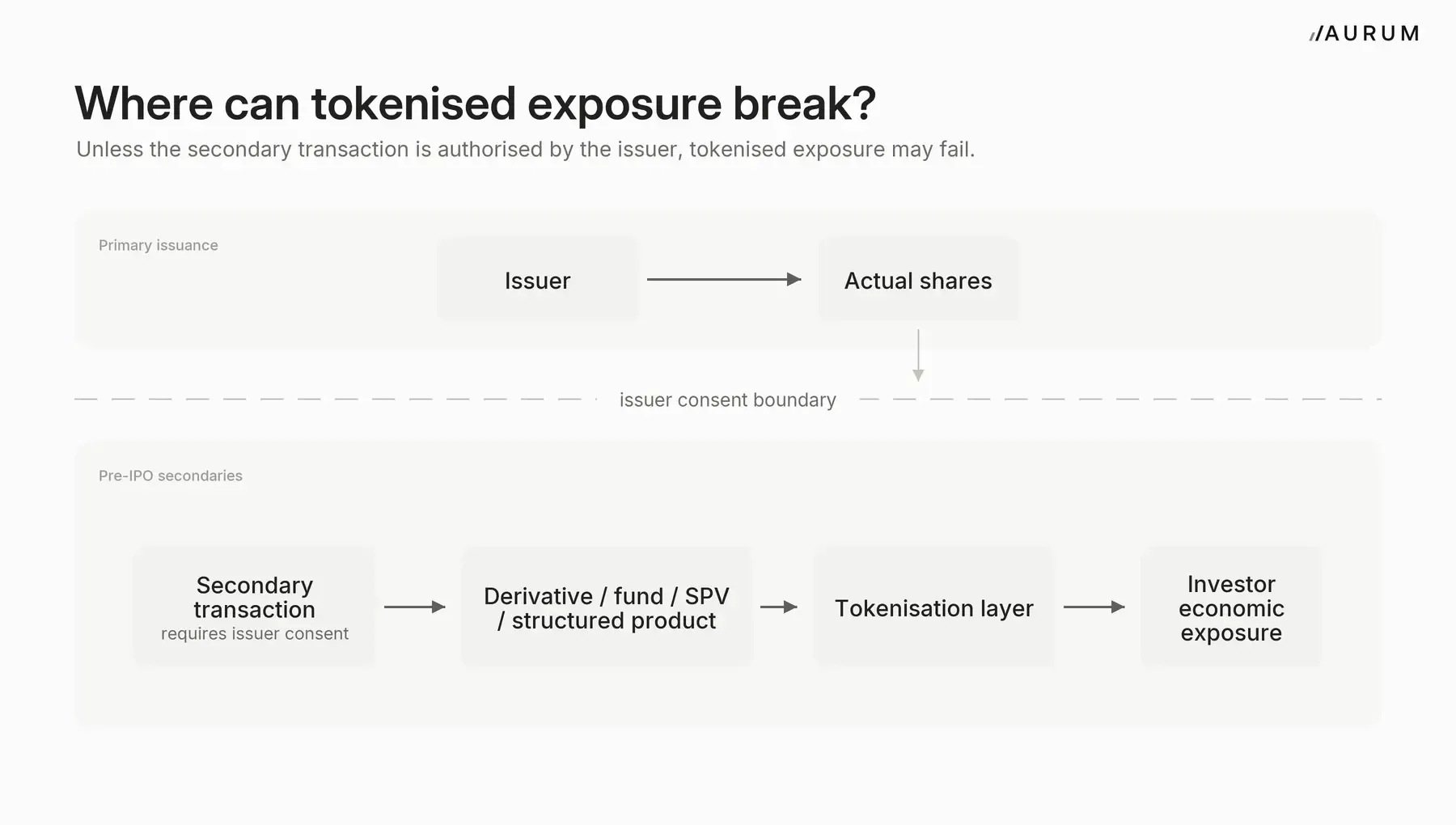

The legal problem is that private-company shares are not public securities waiting to be wrapped. They sit inside an issuer-controlled perimeter: the cap table, transfer agent records, board approvals, and resale restrictions. Outside that perimeter, secondary sellers, SPVs, token platforms and derivative structures can create economic exposure to the company’s value. But that exposure usually depends on an upstream secondary transaction or hedge package – a share transfer, SPV interest, fund unit, forward contract or similar right. If that upstream transaction required issuer consent and the issuer refuses to recognise it, the derivative or tokenised product may lose the asset link that gives it economic substance.

In practical terms, most unauthorised pre-IPO stock tokens should be analysed less as “tokenised shares” and more as intermediary claims whose value depends on whether the issuer recognises the upstream transfer, SPV position or hedge.

This article uses “pre-IPO secondary exposure” to mean secondary or synthetic exposure to existing private-company securities before an IPO. It does not address issuer-led primary financing rounds where the company itself issues securities under approved transaction documents.

This article uses “pre-IPO secondary exposure” to mean secondary or synthetic exposure to existing private-company securities before an IPO. It does not address issuer-led primary financing rounds where the company itself issues securities under approved transaction documents.

What Happened

On February 11, 2026, Anthropic published a support notice on unauthorised stock sales and investment scams, later updated in May 2026. The notice says that sales or transfers of Anthropic stock, or interests in Anthropic stock, require approval by Anthropic’s board of directors and that unapproved transfers will not be recognised on the company’s books and records. It also says that SPVs are not permitted to acquire Anthropic stock, that offers to invest in Anthropic’s past or future financing rounds through an SPV are prohibited, and that third parties claiming to sell Anthropic shares through direct sales, forward contracts, tokenised securities or other mechanisms may be fraudulent, unauthorised or offering exposure that has limited or no value if Anthropic’s transfer restrictions prevent recognition of the underlying transaction.

Anthropic is trying to close unauthorised routes into its cap table before a larger financing or IPO event.

OpenAI had already declared a similar position in its July 16, 2025 policy on unauthorised OpenAI equity transactions. OpenAI says all OpenAI equity is subject to transfer restrictions and cannot be directly or indirectly transferred without written consent. It specifically identifies sales of equity, investments in SPVs that own OpenAI equity, tokenised interests in OpenAI equity or in an SPV holding OpenAI equity, and forward contracts or other purported economic interests. OpenAI says it does not endorse or participate in those unauthorised transactions, that they may result in invalidation of the underlying equity, and that transfers may violate US federal or state securities laws.

Four Ways Pre-IPOs Are Usually Structured

Pre-IPO secondary exposure is usually built through four routes: direct secondary purchase, SPV or fund exposure, synthetic derivative exposure, and securitised or structured-product exposure. These routes are often described with the same retail language even though the instruments, claims and failure modes are different.

In its January 28, 2026 Statement on Tokenized Securities, SEC staff distinguishes issuer-sponsored tokenized securities from third-party tokenized securities, and then separates third-party models into custodial and synthetic structures. Most pre-IPO secondary exposure products sit much closer to the third-party custodial or synthetic side of that taxonomy.

The practical question is therefore what the investor actually receives and what upstream asset or hedge supports that claim.

Route 1 – Direct Purchase

The first route is a direct secondary share purchase. It is the cleanest structure where the transfer is authorised and the buyer becomes a direct recognised and registered holder.

Route 2 – SPV

The second route is SPV or fund exposure. The vehicle may hold shares, convertible notes, fund interests or a contractual right against another holder. Investors buy interests in the vehicle rather than shares of the private company. This can be legitimate where the vehicle and its upstream position are properly authorised. The problem starts when the vehicle lacks issuer consent, cannot prove title, has acquired only a derivative claim, or is used to distribute private-company exposure to a broad audience that would not be eligible for a direct private placement.

It is important to understand that SPVs are not inherently defective. They are widely used in private markets. The legal risk arises where the SPV’s upstream acquisition, beneficial ownership chain, investor distribution or further transfer conflicts with the issuer’s governing documents or approval rights.

Route 3 – Synthetic Exposure

The third route is synthetic derivative exposure. This includes forward contracts, perpetual futures, contracts for difference and similar instruments referencing a private company’s valuation or eventual IPO price. These arrangements create economic exposure without transferring the underlying shares themselves.

Route 4 – Securitised Exposure

The fourth route is securitised or structured-product exposure. Here, an issuer offers notes, certificates or other debt-linked instruments whose redemption value is linked to OpenAI, Anthropic, SpaceX, xAI or a basket of private-company valuations. The investor typically acquires a security issued by the product issuer itself, rather than a direct claim against the referenced private company.

The third and fourth routes also raise securities, derivatives and financial-instrument classification issues. In the EU, UK and US, a tokenised derivative, note or certificate referencing private-company value is not outside the regulatory perimeter merely because it is distributed on-chain or described as a token.

Tokenisation then sits as an additional distribution and settlement layer. It may improve recordkeeping, fractionalisation, transfer mechanics and market access.

Why Private Companies Restrict Transfers Before an IPO

Late-stage private companies control transfers for practical, legal and strategic reasons. A company approaching an IPO wants a clean cap table, identifiable holders, enforceable lock-ups, controlled information flows and a transfer history that underwriters, auditors, transfer agents and exchanges can diligence. If a chain of SPVs and tokenised instruments sits around the shares, the issuer may not know who has economic exposure, who may claim rights after the IPO, whether securities-law exemptions were respected, or whether a disputed transfer could become a closing condition problem.

There are also fraud-control concerns. When a private company becomes highly sought after, unauthorised sellers may offer shares or indirect interests they do not actually own, exaggerate confirmed allocations, present SPV or derivative exposure as direct share ownership, or sell access through layered structures with opaque and excessive fees. Public warnings from issuers are often intended to distinguish legitimate channels from scams, misrepresentation, and fee-driven syndication, especially where investors may commit funds based more on the company’s name than on a verified ownership claim.

From a regulatory perspective, under US securities law, private-company shares are often restricted securities. The SEC’s private secondary markets guidance explains that securities issued in exempt offerings are typically illiquid and not freely tradeable. The SEC’s Rule 144 investor guidance similarly notes that restricted securities acquired in private placements cannot simply be resold into the public market unless the resale is registered or an exemption is available.

Issuer consent is a separate layer. Delaware General Corporation Law Section 202 permits certain transfer restrictions where properly adopted and noticed. In practice, the decisive point is whether the company and its transfer agent will recognise the buyer as a legitimate holder.

However, an issuer’s refusal to consent to or register a secondary transfer is not final in every case. Under Section 202, enforceability turns on the restriction itself, how it was adopted, whether it was properly noticed or known, and what the charter, bylaws, stockholder agreements, side letters and transfer documents actually say. A buyer’s ability to challenge the refusal or seek relief against the issuer would depend on those documents and facts, including prior approvals, issuer communications, course of dealing, waiver or acquiescence.

What This Means for Pre-IPO Secondary Markets, Stock Tokens and Synthetic Exposure

The immediate effect is likely to be a sharper split between authorised and unauthorised access.

This should not be read as a categorical rejection of SPVs. In very large private rounds, issuer-approved co-invest vehicles and SPVs can be necessary capital-formation infrastructure. The pressure falls on unauthorised syndication: nested vehicles, unclear allocation chains, excessive access fees and retail-style distribution that the issuer has not reviewed and from which they want to distance from.

Unauthorised SPVs will face more scrutiny. Investors will increasingly ask for evidence of board approval, transfer-agent recognition, shareholder-agreement compliance, rights-of-first-refusal clearance, side-letter terms, proof of beneficial ownership, and restrictions on further transfers.

For tokenholders, the key points are recourse and transparency. A product may be marketed as exposure to a famous private company, while the legal asset is a high-risk and potentially illiquid claim against a platform, note issuer, fund, SPV or derivative counterparty. That is not the same as a claim against the referenced private company. If the upstream secondary transaction is not recognised, the tokenholder’s practical position depends on the product terms, the hedge documents, the issuer’s credit, custody arrangements, valuation methodology, redemption mechanics and whether the platform has promised any buyback or liquidation right.

The Robinhood/OpenAI dispute shows how this confusion can arise in practice. On June 30, 2025, Robinhood announced stock and ETF tokens in the EU, describing them as a way for eligible European customers to gain exposure to US equities. Robinhood’s private-company promotion terms described the OpenAI and SpaceX tokens as derivative contracts with Robinhood Europe, said holders did not receive rights in actual company shares or hedge assets, and said the SpaceX token was hedged through fund units in an SPV holding SpaceX preferred shares while the OpenAI token was hedged through fund units in an SPV holding OpenAI convertible notes.

This enables the tokenholder to receive price exposure without voting rights, information rights, inspection rights, direct issuer recourse, transfer-agent recognition or any right to receive the underlying private-company shares.

OpenAI publicly objected in July 2025, saying that the OpenAI tokens were not OpenAI equity and that no equity transfer had been approved. There does not appear to have been a reported OpenAI v Robinhood court case. But Robinhood later described the structural risk in its 2025 Form 10-K/A: private-company issuers may object to synthetic instruments that reference their securities, may assert that an SPV interest is invalid, void or unenforceable, and that this could impair the SPV’s rights to the underlying securities and prevent Robinhood from effectively hedging customer tokens.

Structuring Considerations

Pre-IPO secondary tokenisation remains viable when structured as a genuine capital-markets product rather than as a branding layer built around private-company scarcity. A credible structure must address several core issues before distribution, including the upstream title or hedge, the holder’s legal rights and recourse, issuer-recognition risk, investor eligibility, transferability, valuation methodology and regulatory classification.

Products that can evidence a recognised upstream position, describe the holder’s claim accurately, disclose the consequences of issuer non-recognition and keep distribution inside the right regulatory perimeter will be in a different category from products that sell private-company exposure mainly through scarcity and implied affiliation. Detailed structuring choices should therefore be resolved through counsel-led product design tailored to the specific instrument, hedge, issuer-recognition pathway and distribution model.

Conclusion

Anthropic and OpenAI have made issuer recognition and investor transparency the central questions for pre-IPO secondary tokenisation: SPVs, funds, notes, derivatives and tokenised instruments can distribute economic exposure, but its legal value depends on the holder’s claim, the upstream title or hedge, issuer recognition and whether investors understand that they may hold a high-risk, potentially illiquid intermediary claim rather than tokenised stock.

How Aurum Can Assist

Aurum advises teams building Next-Generation Finance products across on-chain capital markets, on-chain asset management, tokenisation and regulated digital asset infrastructure.

Related publications

DeFi Interface Regulation: Building a Compliant Frontend. Legal Risks & Compliance Checklist

Partner

Subscription Compliance by Design: How to Build a Transparent Subscription Flow in B2C Digital Products

Valeriia Sych

Junior Associate

LinkedIn Marketing Legal Checklist: What Businesses Should Check Before Launching a Campaign

Tetiana Kontariova

Associate

Cold Outreach Compliance: What to Check Before Sending Emails or Using AI Tools

Tetiana Kontariova

Associate